By Mirek Gruna, Regional Chief Commercial Officer, EMEA

The UK’s carried interest reforms, announced in 2024 and now shaped through Finance Bill 2026, will bring carried interest within the income tax regime from 6 April 2026. Carried interest will be taxed as deemed trading income and subject to an effective tax rate of 34.1%. Jersey and Guernsey are now drawing attention from GPs as jurisdictions of choice for restructuring thanks to their mature financial services ecosystems, tax efficiency, and proximity to London.

What is carried interest?

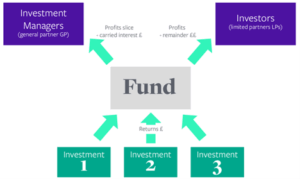

Carried interest is a share of the profits that investment managers receive as compensation for successfully increasing the value of investors’ capital. Rules governing carried interest are typically written into a fund’s constitutional documents.

Key points:

- Carried interest is performance-based compensation, not a guaranteed fee

- Managers usually earn carried interest only after investors receive back their original capital and often a minimum preferred return (the “hurdle rate”)

- A common carried interest share is 20% of the fund’s profits, though it varies by fund

- Aligns the interests of fund managers with investors, as managers profit more when the fund performs well

What are the UK carried interest tax changes from April 2026? Finance Bill 2026 highlights

Exclusive charge mechanics

What changed: A key policy of the new regime is that the carried interest income tax charge should serve as the primary UK tax charge on carry. Finance Bill 2026 refines the drafting to address scenarios where other UK tax charges could arise first – for example, where carry sits in a retention account. It also addresses scenarios where carry profits arise to someone other than the executive (for example, certain personal holding arrangements).

What this means for GPs:

- Less uncertainty around “double charge” mechanics: But you still need to map out where tax could arise in the structure and when

- Award timing still matters: The updates retain scope for HMRC to seek tax at the point carry is awarded if it has value at that time

- Relief may require a claim: If another person/vehicle has already borne UK tax on the carry, the executive may be able to reduce taxable profits under the new regime, but that relief is not automatic. Documentation and governance trails are more important than ever

Average holding period refinements

What changed: The average holding period (AHP) rules determine whether carry is “qualifying” (eligible for the 34.1% effective rate outcome) or “non-qualifying.” Finance Bill 2026 includes additional amendments aimed at making AHP calculations more workable for fund types that have historically struggled – particularly private credit, funds-of-funds (FOFs) and certain real estate scenarios.

What this means for GPs:

- Better treatment for credit strategies: Including restructurings and loan-relationship-style arrangements

- Clarity for FOFs: Qualifying investments have been extended to include direct co-investments

- Conditionally qualifying carry: More room to rely on “reasonable to assume” logic earlier in a fund’s life, reducing the risk of mismatches and late-payment interest in scenarios where AHP evolves over time

- Operational workload remains high: While the rules may be more workable, they still involve ongoing calculation, monitoring and reporting needs, especially for executives holding carry across multiple funds

Territorial limitations

What changed: Territorial scope has been a major concern because the new regime treats carry like trading income, raising questions about how far UK services could pull non-UK residents into the UK tax net. Finance Bill 2026 makes changes intended to improve how the UK workdays safe harbour operates for qualifying carry and refines how the “relevant period” is measured.

What this means for GPs:

- More usable safe harbour logic: In situations where carry ultimately becomes qualifying, there is less risk that non-UK executives must do heavy AHP work to establish they’re below UK workday thresholds

- Cleaner linkage to the executive’s role: This should reduce the chance that carried interest unrelated to a UK role is dragged into UK tax

What should UK-based fund managers do now?

In our experience, the highest-impact tax regime planning tends to focus on three areas:

1. Residency and working patterns

Your location and working pattern matter more than fund domicile when assessing exposure and outcomes under the new regime.

2. Carry vehicle governance and documentation

If carry is routed through vehicles or holding arrangements, keep your governance trail consistent. Document who holds what, when entitlements arise, and how distributions flow.

3. Implementation risk

Even well-designed plans can fail if ongoing administration isn’t up to the task. Inconsistent reporting, entity sprawl without governance, and cross-border coordination are all common failure points to look out for.

Considerations for asset owners

For individuals awarded carry, early structuring advice is essential. While carry may have limited value at the point of award, putting the right vehicle in place from the outset minimises tax leakage as the asset grows.

Where other private equity opportunities arise alongside carry, the situation grows more complex:

- Tracking commitments and distributions

- Managing liquidity

- Ensuring correct reporting

- Navigating cross-border tax issues

Structures should evolve over time, but building on solid foundations from the start makes the complexity easier to manage and minimises exposure.

Why Jersey and Guernsey appeal to UK-connected fund managers

Under the new regime, GPs with more location independence are looking for jurisdictions that support a workable operating model outside the UK. Jersey and Guernsey appeal for reasons that extend beyond tax. For UK-connected GPs and carry holders, the appeal is often a combination of tax efficiency, proximity to the UK, and ecosystem maturity.

Clear personal income tax baseline

In the Channel Islands, the standard income tax rate is 20% of assessable income. As always, individual circumstances matter. Allowances, residency categories, and other rules can change outcomes, but the clear baseline keeps Jersey and Guernsey at the top of many shortlists.

Proximity to London

Many firms will keep meaningful operations in London because it remains a global hub for capital and talent. But the Channel Islands can support a model that preserves UK connectivity while aligning residency and operations with a tax efficient framework.

Mature fund and entity ecosystem

In a multi-vehicle structure, getting the operational details right is critical. Accounting, entity administration, reporting, investor communications, governance and cross-border coordination all require expertise and supporting infrastructure, and the Channel Islands’ established maturity in these areas is a significant draw.

How Jersey and Guernsey structures can be used in practice

One common misconception is that moving a fund to Jersey or Guernsey automatically changes the UK tax outcome for carried interest. In reality, many UK-based managers keep core fund structures broadly consistent, while adjusting the individual and operational pieces around carry.

At a high level, a Channel Islands approach often looks like this:

- Carry vehicle and administration: The carried interest vehicle can be established and administered in Jersey or Guernsey, creating a stable operational base for governance, distributions and reporting

- Entity and reporting discipline: SPVs or co-investment vehicles and related entities are administered within a consistent operating framework, reducing fragmentation risk

- Individual-level alignment: Where relocation is part of the plan, the structure is supported by the practical realities of where carry recipients live and work

In other words, fund managers must focus beyond the structure itself on ongoing administration, ensuring operations run cleanly year after year.

What about the Dubai International Financial Centre (DIFC)?

Dubai is also a popular jurisdiction for tax efficiency, particularly for internationally mobile principals weighing a broader shift. Many UK-based GPs view the decision as two distinct operating models:

- Channel Islands: Maintain UK connectivity with an established governance and administrative ecosystem

- Dubai/DIFC: A deeper lifestyle and operating footprint shift, potentially alongside wider business decisions

FAQs

When do the UK carried interest tax changes take effect?

The revised regime takes effect from 6 April 2026.

What does “carried interest taxed as deemed trading income” mean?

Carried interest will generally be taxed within an income tax framework as profits of a deemed trade, bringing Income Tax and Class 4 NICs into scope for affected UK taxpayers.

What changed in Finance Bill 2026 compared to earlier drafts?

Key refinements include improvements around the “exclusive charge” concept and overlap risk, targeted changes to AHP mechanics (notably for credit and FOF structures), and clarified territorial limitations for non-UK residents.

Does moving the fund to Jersey or Guernsey avoid UK carried interest tax?

The decisive factor is usually where carry recipients live and work, alongside how carry vehicles and governance are administered. Fund domicile can be relevant for many reasons, but it does not automatically determine UK carry tax exposure under the new regime.

How we can help

IQ-EQ supports fund managers globally with fund services designed for complex, multi-entity structures and cross-border coordination. With $857bn in assets under administration, we operate across 24 jurisdictions and share decades of expertise.

Key strengths include:

- Technology: Scalable solutions built to meet your needs, from end-to-end managed data services to fund accounting and data visualisation tools

- GP experience: Services ranging from full outsourcing and co-sourcing to a direct cost model and lift-outs. We’ve also invested in a deep technical knowledge bench to solve complex problems

- LP experience: We assure investors and stakeholders with our robust control and compliance environment. We onboard investors in multiple jurisdictions, perform AML/KYC and monitor investors through the life of a fund